Also, you're letting sellers understand you're a serious and certified purchaser. Often, if there's competitors for a house, buyers who have their funding in place are preferred due to the fact that it shows the seller you can afford the home and are prepared to buy. We'll also go through the pre-approval procedure a bit more in the next section. You set up to pay back that money, plus interest, over a set period of time (called a term), which can be as long as 30 years. To make certain that you repay the cash you borrowed, you put your home up as collateralso if you stop making payments, the bank can take your house far from you in a procedure called a foreclosure.

If you take out a mortgage that isn't right for you, leading to foreclosure, you'll not only have to moveand in general wait in between three and 7 years prior to you are permitted to buy another homebut your credit rating will likewise suffer, and you could be struck with a substantial tax costs.

That's where we are available in. The business that provide you with the funds that you need are referred to as "loan providers." Lenders can be banks or home loan brokers, who have access to both large banks and other loan lenders, like pension funds. In 2012, the greatest loan providers in the country consisted of Wells Fargo, Chase and Bank of America.

You wish to make sure that whoever you work with directly has a track record for being trustworthy and efficient, due to the fact that any hold-ups or problems with closing on a sale will only cost you more cash. Government loans are available through the Federal Housing Administration, but the availability of loans differs depending on where you live.

Our What Is The Truth About Reverse Mortgages Ideas

Mortgage lenders do not provide numerous thousands of dollars to simply anyone, which is why it's so important to keep your credit history. That rating is one of the main manner ins which loan providers evaluate you as a reputable borrowerthat is, somebody who's likely to pay back bluegreen timeshare the cash in complete.

Some lending institutions may decline your application if you have a lower credit rating, but there isn't a universal cutoff number for everyone. Rather, a lower credit rating indicates that you may wind up with a greater interest rate. A charge you may sell timeshare see enforced by a loan provider is one for "points." These in advance fees (they typically exercise to be about 1% of the loan quantity) are usually a type of pre-paid interest.

Points are paid at closing, so if you're trying to keep your upfront costs as low as possible, choose a zero-point choice. With a home mortgage, you'll pay the principal, interest, taxes and insuranceall of which are commonly referred to as PITI. Keep in mind that unless you are a high-risk borrower, you can pick to pay taxes and insurance separately from your home loan, which will provide you a lower home loan payment.

Here's how each component of PITI works: This is the original quantity that you borrowed to pay your home loan (what kind of mortgages are there). The bank chooses just how much it will provide you based upon aspects like earnings, credit and the quantity you plan to give for a deposit. If your down payment is less than 20% of the home's price, the bank might consider you to be a riskier lender and either charge you a greater interest rate or need that you buy private mortgage insurance coverage, commonly referred to as PMI.

The Buzz on What Is The Current Libor Rate For Mortgages

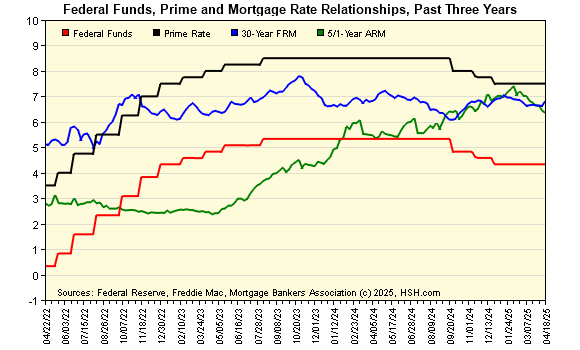

When you get a home mortgage, you accept a rates of interest, which will determine how much you pay a lending institution to keep lending. It's revealed as a portion: 5% to 6% is thought about rather basic, but the rates depend highly on a person's situationincome, creditas evaluated by the lending institution.

Residential or commercial property taxes go towards supporting city, school district, county and/or state facilities, and you can pay them together with your mortgage. They're expressed as a portion of your property worth, so you can approximately approximate what you'll pay by browsing public records for the property taxes for nearby houses of similar value.

Any payments reserved for property owner's insurance coverage to secure against fire, theft or other disasters are likewise kept in an escrow account. (Once again, this is something that you can choose out of escrowing, unless you're a high-risk customer.) If you're a high-risk borroweror if you do not have the 20% down paymentyou're also required to have private home mortgage insurance coverage (PMI), which helps guarantee that the loan provider will get money back if you can't pay it for any reason.

Keep in mind that PMI is suggested to secure the loan provider, not the borrowerso it won't bail you out if you default on your payments. Home mortgages are structured so that the percentage of your payment that approaches your principal shifts as the years pass. At initially, you're paying primarily interest; eventually, you'll pay primarily primary.

Which Of The Following Statements Is Not True About Mortgages? Fundamentals Explained

There are a few various types of common home loans: This is the most popular payment setup for a home loan - what are today's interest rates on mortgages. It means that the borrower will pay a "repaired" interest rate for the next thirty years. It's an attractive possibility because homeowners will pay the specific very same amount every month. Set home mortgages are best for homebuyers who buy when rates of interest are low or on the rise, are counting on a foreseeable payment and who plan to remain in the house for a long time.

These are best for homeowners who https://259716.8b.io/page2.html desire to pay off their mortgages and construct equity rapidly. Rates of interest for 15-year set home loans normally also carry lower rate of interest than 30-year home mortgages. The interest rates on adjustable rate mortgages are changed at predetermined intervals to show the present market. Some home loans are a combination of repaired and adjustable: for the first three, 5 or seven years, the rate will remain repaired, and then be adjusted yearly for the duration of the loan.

This kind of loan might be best for you if you prepare to live in your house for roughly the very same length of time as the original fixed term. Remember Long prior to you actually request a mortgage, you can start building your reliability by developing great credit, and accumulating cost savings for a down payment.

A home loan is a loan secured to purchase home or land. The majority of run for 25 years but the term can be shorter or longer. The loan is 'protected' against the value of your home up until it's settled. If you can't maintain your repayments the lending institution can repossess (reclaim) your house and sell it so they get their cash back.

Getting The What Is The Current Libor Rate For Mortgages To Work

Likewise, believe about the running costs of owning a house such as home expenses, council tax, insurance and maintenance. Lenders will desire to see evidence of your earnings and specific expenditure, and if you have any financial obligations. They might request details about family costs, child upkeep and individual expenses.