Reverse home loans were designed for older people to tap their house equity to increase their monthly cash flow without the problem of regular monthly payments. westley morgan To get approved for a reverse mortgage, you need to be at least 62 years of ages. Prospective customers also should go through a home counseling session to make sure that they completely comprehend the ins and outs of a reverse home loan.

Financial investment homes and villa do not certify. You must live at the residential or commercial property for more than six months of the year. Normally, you can't obtain more than 80% of your house's value, up to the FHA optimum of $726,525 for 2019. Typically, the older you are, the more you can obtain.

" So, they are taking a look at getting a loan that deserves 68% of their house's worth." You're likewise required to pay home taxes, house owner's insurance coverage and mortgage insurance coverage premium in addition to preserving your home. Your loan provider will evaluate whether you have enough disposable earnings to fulfill these obligations. In many cases, melanie rowland poynter lenders may need that a few of the equity from the reverse home mortgage is reserved to pay those expenditures moving forward.

That indicates the loan balance grows in time. For circumstances, you may borrow $100,000 upfront, however by the time you pass away or sell your home and relocation, you will owe more than that, depending upon the interest rate on the reverse home mortgage. There are five ways to have the funds from a reverse home mortgage distributed to you: You can take the cash you're entitled to upfront.

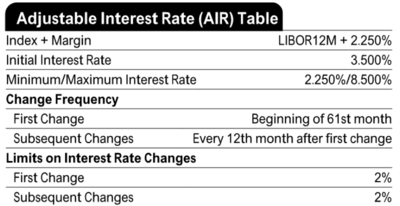

Typically, these kinds of reverse home loans featured a set rates of interest on the outstanding balance. You can receive the funds as a regular monthly payment that lasts as long as you remain in the house. This reverse mortgage generally has an adjustable interest rate. You can get funds monthly for a specified period.

The rate of interest is likewise adjustable. Under this scenario, you don't take any cash at all. Instead, you have a line of credit you can make use of at any time. The credit line also grows in time based upon its adjustable rate of interest. You can also integrate the above alternatives.

How Do Mortgages Work Condos Fundamentals Explained

If you wish to change the alternatives later on, you can do this is by paying an administrative cost, Stearns stated. If you want to stay in your house for a very long time in your retirement and have no desire to pass down your house to your kids, then a reverse mortgage may work for you.

The perfect reverse home loan debtors also are those who have developed considerable and varied retirement cost savings. "But they have substantial wealth in their home and they desire as much spendable funds in their retirement as possible," said Jack Guttentag, professor of financing emeritus at the Wharton School of the University of Pennsylvania.

If you don't completely understand the home loan, you should likewise avoid http://kittanhue6.booklikes.com/post/3466860/how-do-uk-mortgages-work-can-be-fun-for-anyone it. "These are complicated products," Nelson said. "It's a mind tornado to think of equity disappearing." If you wish to leave your house to your children after you die or move out of the home, a reverse home loan isn't a great option for you either.

If you don't make your property tax and insurance coverage payments, that could trigger a foreclosure. Likewise, if you don't react to yearly correspondence from your lender, that might likewise trigger foreclosure procedures. Regrettably, small violations like not returning a residency postcard, missing tax or home insurance payment, or poor maintenance can cause foreclosure rapidly.

If your spouse is not a co-borrower on the reverse home loan when you die, what happens next depends upon when the reverse mortgage was secured. If it was secured on or after Aug. 4, 2014, a non-borrowing spouse can remain in the home after the borrower dies however does not get any more of the loan funds as long as he or she meets these eligibility requirements: Married to the borrower when the loan closed Remain wed until the borrower dies Named as a non-borrowing spouse in the loan files Live and continue to live in the house as the primary residence Able to prove legal ownership after the borrower dies Pay the taxes and insurance coverage and maintain the house's upkeepThe debtor and spouse need to accredit at the loan's closing and every following year that they are still married and the partner is an eligible non-borrowing partner.

If these conditions aren't fulfilled, the partner can deal with foreclosure. For reverse mortgages taken out prior to Aug. 4, 2014, non-borrowing partners have less protections. The lender does not have to enable the non-borrowing partner to remain in the house after the borrower dies. A borrower and his or her spouse can ask a lending institution to apply to HUD to enable the non-borrowing partner to remain in the house - how do mortgages work when building a home.

The Only Guide for How Do Mortgages Work When Building A Home

Some loan providers provide HECM lookalikes but with loan limits that surpass the FHA limit. These reverse mortgages frequently resemble HECMs. how do fixed rate mortgages work. However it is necessary to understand any distinctions. Know how your reverse home loan expert earns money. If paid on commission, beware if the expert encourages you to take the optimum upfront money, which means a larger commission.

" Individuals do not look at reverse home loans till it ends up being a need. They can be desperate." There are other ways for elders to unlock the equity they developed in their houses over the years without getting a reverse home loan. If you require the equity for your retirement years, it's essential to consider all options.

The disadvantage is quiting the family house. However potential advantages include moving closer to family and purchasing a house better for aging in location. You can either re-finance or take out a new home mortgage if you don't have an existing one and money out a few of the equity.

You could also borrow against your house equity using a house equity loan or line of credit. A loan permits you to take a lump amount upfront that you repay in installment payments. With a line of credit, you can borrow from it at any time, approximately the maximum amount.

A reverse mortgage loan, like a traditional home loan, allows homeowners to obtain cash using their home as security for the loan. Likewise like a standard home loan, when you get a reverse home loan, the title to your house remains in your name. However, unlike a conventional home mortgage, with a reverse mortgage loan, borrowers do not make regular monthly home loan payments.

Interest and charges are contributed to the loan balance monthly and the balance grows. With a reverse mortgage loan, homeowners are required to pay real estate tax and property owners insurance, use the property as their principal home, and keep their house in great condition. With a reverse home loan, the quantity the house owner owes to the loan provider goes upnot downover time.

5 Simple Techniques For How Do Fixed Rate Mortgages Work

As your loan balance boosts, your house equity decreases. A reverse home loan is not totally free money. It is a loan where obtained cash + interest + costs every month = rising loan balance. The property owners or their beneficiaries will eventually need to pay back the loan, usually by selling the house.